Model evaluation error metrics#

To evaluate different quality control methods, their results can be methodologically compared to raw data. For this, we provide several evaluation metrics which are desgined for skewed timeseries data. In the following, we explain three example evaluation metrics.

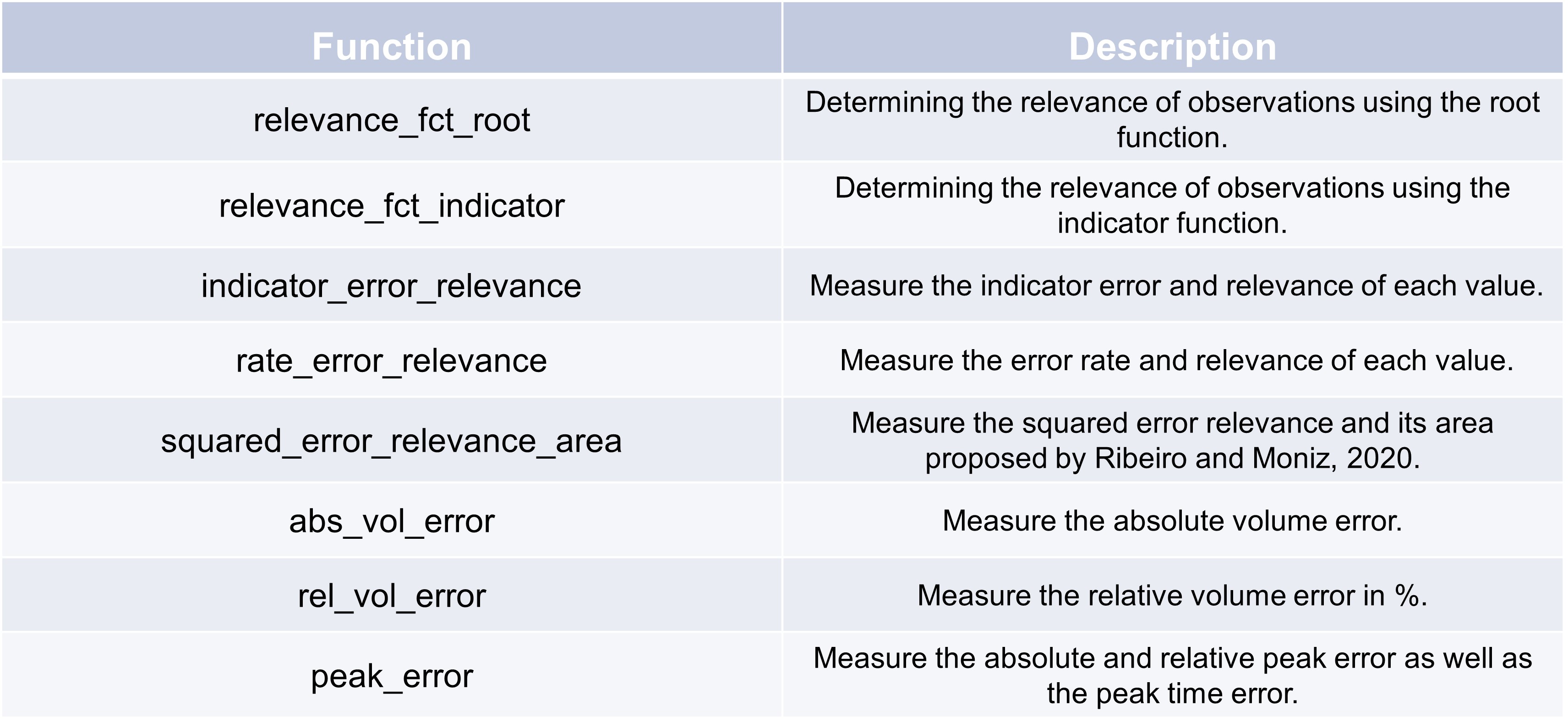

relevance_fct_root and relevance_fct_indicator can be used to determine the relevance of observations. They are

usually used within evaluation functions for a sample weighting.

indicator_error_relevance, rate_error_relevance, and squared_error_relevance_area can bu utilized

similar to, e.g. the MSE metric from scikit-learn for an evaluation of the whole dataset (maybe with sample weighting).

The last three evaluation metrics from the table, abs_vol_error, rel_vol_error, and peak_error

are usually applied on an event basis.

Dataset-based evaluation#

>>> y_gt = pd.Series([0, 1, 2, 1.25])

>>> y_pred = pd.Series([0, 0, 4, 1.26])

>>> print("Indicator error relevance + no weight. \t\t%.2f" % TSCC.assessment.indicator_error_relevance(y_gt, y_pred, (-float("inf"), 1), lambda y_gt: pd.Series([1] * len(y_gt))))

>>> print("Indicator error relevance + ind. weight. \t%.2f" % TSCC.assessment.indicator_error_relevance(y_gt, y_pred, (-float("inf"), 1), TSCC.assessment.relevance_fct_indicator, (1.25,float("inf"))))

>>> print("Indicator error relevance + root weight.\t%.2f" % TSCC.assessment.indicator_error_relevance(y_gt, y_pred, (-float("inf"), 1), TSCC.assessment.relevance_fct_root))

>>> print("MSE + ind. weight.\t\t\t\t%.2f" % sklearn.metrics.mean_squared_error(y_gt, y_pred, sample_weight = TSCC.assessment.relevance_fct_indicator(y_gt, (1.25, float("inf")))))

>>> print("Rate error relevance + ind. weight.\t\t%.2f" % TSCC.assessment.rate_error_relevance(y_gt, y_pred, TSCC.assessment.relevance_fct_indicator, (1.25,float("inf"))))

>>> print("SERA + root weight.\t\t\t\t%.2f" % TSCC.assessment.squared_error_relevance_area(y_gt, y_pred, TSCC.assessment.relevance_fct_root(y_gt))[0])

Indicator error relevance + no weight. 0.75

Indicator error relevance + ind. weight. 0.50

Indicator error relevance + root weight. 0.85

MSE + ind. weight. 2.00

Rate error relevance + ind. weight. 0.50

SERA + root weight. 5.00

Our data set to be evaluated consists of a ground truth series and a prediction series.

The first evaluation metric is the indicator_error_relevance metric without a weighting ob observations (equal weights).

The result is 0.75, because 3/4 of the observations are within the given maximal deviation 1 of y_gt

and y_pred. The second example also uses indicator_error_relevance metric but with a weighting by

relevance_fct_indicator. The binary weighting leads to a disregarding of observation 0 and 1. Observation 3 is

not withing the given maximal deviation, observation 4 is. The result is therefore 0.5. indicator_error_relevance

with the relevance_fct_root works in the same way besides its different observation weighting.

We also used the regular scikit-learn mean_squared_error with our custom relevance function.

Event-based evaluation#

First, a data set containing several events is created. Then, events are isolated using the TSCC.exploration.getEvents function. At last, different event-based evaluation metrics such as the absolute volume error are computed.

import pandas as pd

import numpy as np

from datetime import datetime, timedelta

# Generate sample data for demonstration

np.random.seed(0)

# Generate timestamps

start_time = datetime(2024, 1, 1)

end_time = datetime(2024, 1, 2)

num_samples = 25

timestamps = pd.date_range(start=start_time, end=end_time, periods=num_samples)

# Generate df_value_raw and df_value_gt using gamma distribution

shape_raw, scale_raw = 2., 10. # Gamma distribution parameters for df_value_raw

shape_gt, scale_gt = 2.5, 10.5 # Gamma distribution parameters for df_value_gt

# Parameters for generating dependent values

mean_shift_raw = 0.2 # Mean shift for df_value_raw

mean_shift_gt = 0.3 # Mean shift for df_value_gt

autoreg_factor_raw = 0.7 # Auto-regressive factor for df_value_raw

autoreg_factor_gt = 0.8 # Auto-regressive factor for df_value_gt

# Generate df_value_raw and df_value_gt with auto-regressive behavior

df_value_raw = np.zeros(num_samples)

df_value_gt = np.zeros(num_samples)

for i in range(1, num_samples):

df_value_gt[i] = mean_shift_gt + autoreg_factor_gt * df_value_gt[i - 1] + np.random.gamma(shape_raw, scale_raw)

df_value_raw = df_value_gt + np.random.normal(0, 5, num_samples)

# Create the DataFrame

df = pd.DataFrame({

'timestamp': timestamps,

'df_value_gt': df_value_gt,

'df_value_raw': df_value_raw,

})

# Display the first few rows of the DataFrame

print(df.head())

timestamp df_value_gt df_value_raw

0 2024-01-01 00:00:00 0.000000 -2.548261

1 2024-01-01 01:00:00 51.688296 49.497924

2 2024-01-01 02:00:00 64.035446 57.771469

3 2024-01-01 03:00:00 105.799679 109.687131

4 2024-01-01 04:00:00 91.905608 83.836119

event_list = TSCC.exploration.getEvents(df.set_index('timestamp')["df_value_gt"],

max_time_dist_from_center = "120t",

center_valley = (70, float("inf")),

center_peak = (100, float("inf")),

event_sum=(500, float("inf")),

event_dist = (0.000001, float("inf"), .3))

for cur_event in event_list:

print("Event characteristics (of ground truth)")

print("Event start:\t\t", cur_event[0])

print("Event end:\t\t", cur_event[1])

print("Event min. intensity:\t%.2f" % cur_event[2])

print("Event max. intensity:\t%.2f" % cur_event[3])

print("Event sum:\t\t%.2f" % cur_event[4])

print()

print("Evaluation results")

df_event = df.query(f'"{cur_event[0]}" <= timestamp <= "{cur_event[1]}"')

ave = TSCC.assessment.abs_vol_error(df_event.set_index("timestamp")["df_value_gt"], df_event.set_index("timestamp")["df_value_raw"])

print("Absolute volume error:\t%.2f" % ave)

rve = TSCC.assessment.rel_vol_error(df_event.set_index("timestamp")["df_value_gt"], df_event.set_index("timestamp")["df_value_raw"])

print("Relative volume error:\t%.2f" % rve)

ape, rpe, pte = TSCC.assessment.peak_error(df_event.set_index("timestamp")["df_value_gt"], df_event.set_index("timestamp")["df_value_raw"])

print("Absolute peak error:\t%.2f" % ape)

print("Relative peak error:\t%.2f" % rpe)

print("Peak time error:\t", pte)

print()

Event characteristics (of ground truth)

Event start: 2024-01-01 06:00:00

Event end: 2024-01-01 10:00:00

Event min. intensity: 94.20

Event max. intensity: 105.61

Event sum: 510.93

Evaluation results

Absolute volume error: -11.14

Relative volume error: -2.18

Absolute peak error: 0.53

Relative peak error: 0.51

Peak time error: -1 days +21:00:00

The output includes an event from 2024-01-01 06:00:00 to 2024-01-01 10:00:00 (based on the criteria set in TSCC.exploration.getEvents).

The absolute volume error of this event is -11.14 units (abs_vol_error), the prediction is 11.14 units less

than the ground truth. The relative error is -2.18`% (``rel_vol_error`).

The APE, RPE and PTE can be retrieved using peak_error.

The absolute peak error of the prediction in contrast to the ground truth is 0.53, the prediction is

therefore 0.53 units greater than the ground truth. The relative peak error is `0.51`%.

And the peak time is 3 hours earlier for the prediction than for the ground truth.